SPECIAL REPORT: AFRICA EMERGING FROM THE PANDEMIC

Thu, 22 April 2021

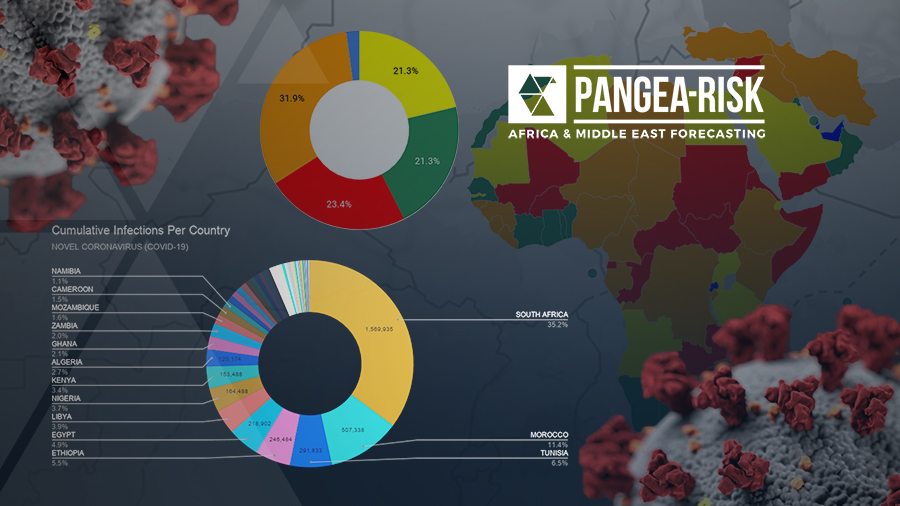

A handful of African countries will begin to emerge from the pandemic this year. Based on the latest economic outlook data and PANGEA-RISK’s updated quantitative country risk ratings, we assess the trajectory of the pandemic in Africa, the road ahead for the vaccination rollout, persistent sovereign debt concerns, and the most likely winners and losers as the continent tentatively steers toward recovery.