SPECIAL REPORT: AFRICA LOBBIES FOR DEBT SWAP TO AVOID WAVE OF SOVEREIGN DEFAULTS

Mon, 04 May 2020

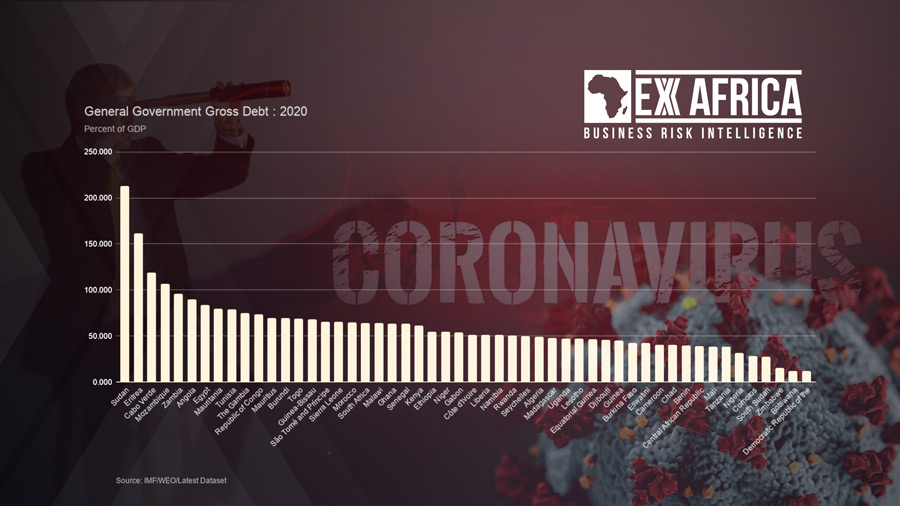

Despite rating agency resistance, Africa wants to convert some of its debt into longer-term instruments in order to head off any risk of default. The extreme instance of Zambia demonstrates the urgency for debt distressed African countries to join a continental effort to restructure loans. Without such an approach, some of Africa’s largest economies will almost certainly default this year.