SPECIAL REPORT: AFRICA’S COMMON MARKETS COMPETE FOR TRADE AND INVESTMENT

Mon, 08 March 2021

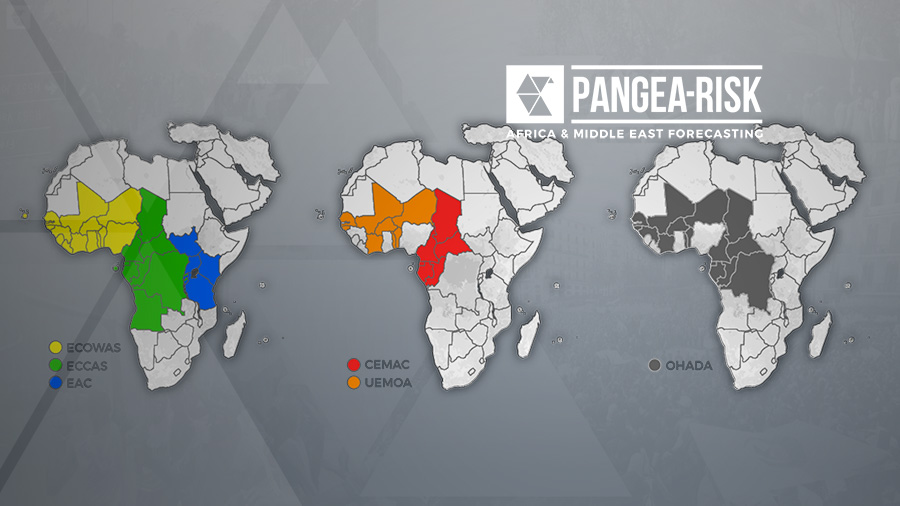

Africa’s regional economic communities, common markets, and currency unions will be crucial to drive a post-pandemic recovery and boost intra-regional trade under the continent’s new free trade pact. While some regional blocs in the East and West are better suited to accelerate integration and take advantage of new trade and investment opportunities, institutions in Central Africa are poorly equipped to enhance their region’s competitive advantage. PANGEA-RISK compares six African regional blocs to determine the criteria for success.