SPECIAL REPORT: COUNTRY RISK 'WINNERS' AND 'LOSERS' FOR 2021

Tue, 05 January 2021

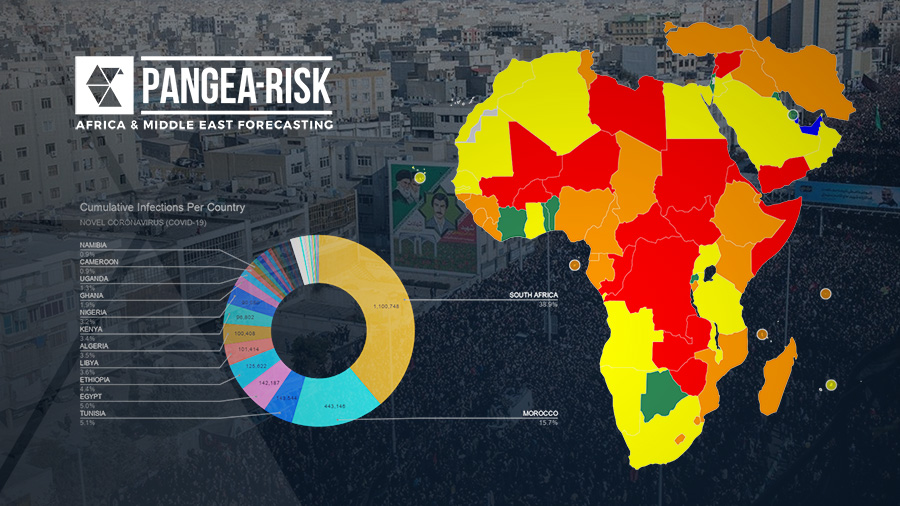

In the coming year, Sudan is likely to make the most significant improvement to its country risk outlook following several recent developments, while Egypt and Iran are also set to make important headway in 2021. However, previous investment favourites Ethiopia and Zambia, alongside Turkey, will see substantial deterioration in their country risk outlook this year. PANGEA-RISK assesses the key drivers of risk in Africa and the Middle East for the year ahead.