SPECIAL REPORT: DEBT RELIEF PROPOSALS FOR AFRICA ARE MAKING LITTLE PROGRESS

Mon, 24 May 2021

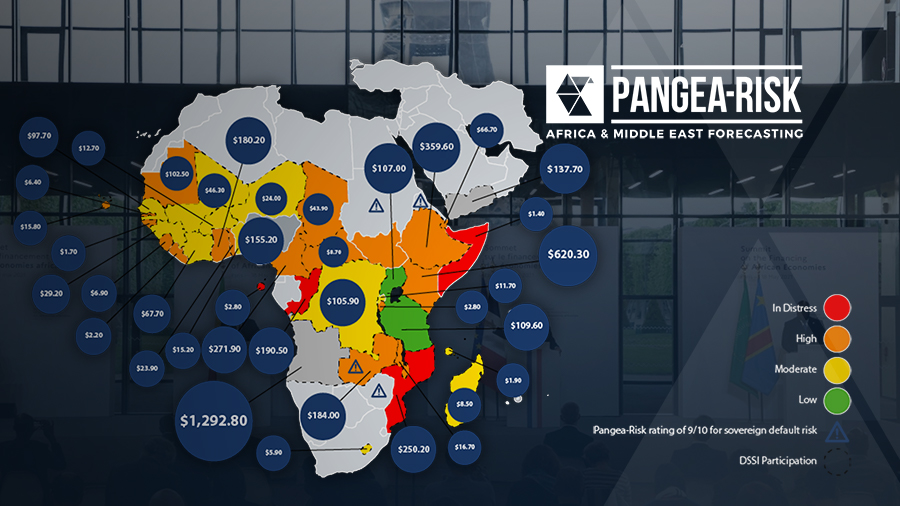

Proposals on how to redirect IMF international reserve assets from developed countries to emerging markets are failing to make headway. The prospect of blanket debt relief in Africa remains remote, while deferred interest on bilateral and concessional loans will become due from next year. Few countries will be able to make such bullet payments on time. Nevertheless, some debt distressed countries are benefitting from case-by-case relief measures and settling of long-held arrears.