SPECIAL REPORT: INVESTMENT AND TECHNOLOGICAL ADVANCES CEMENT UAE’S POSITION AS GLOBAL COMMODITY HUB

Wed, 08 February 2023

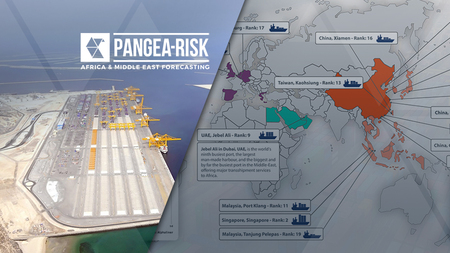

The United Arab Emirates’ (UAE) container ports are expanding rapidly, emerging at the top of global indices in terms of volume growth and efficiency. Dubai, specifically, endeavours on becoming the financial and trading centre of the Middle East region. It intends to compete as a trading hub with New York, London, Hong Kong, and Singapore. And there are signs that the emirate might not be far off from achieving this goal. Despite a gloomy outlook for world trade in 2023, the UAE’s growing role as an emerging market and a global transhipment hub is set to accelerate, supporting economic growth, and attracting investment.