SPECIAL REPORT: POSITIVE RISK TRENDS TO ANTICIPATE IN AFRICA AND THE MIDDLE EAST IN 2023

Mon, 09 January 2023

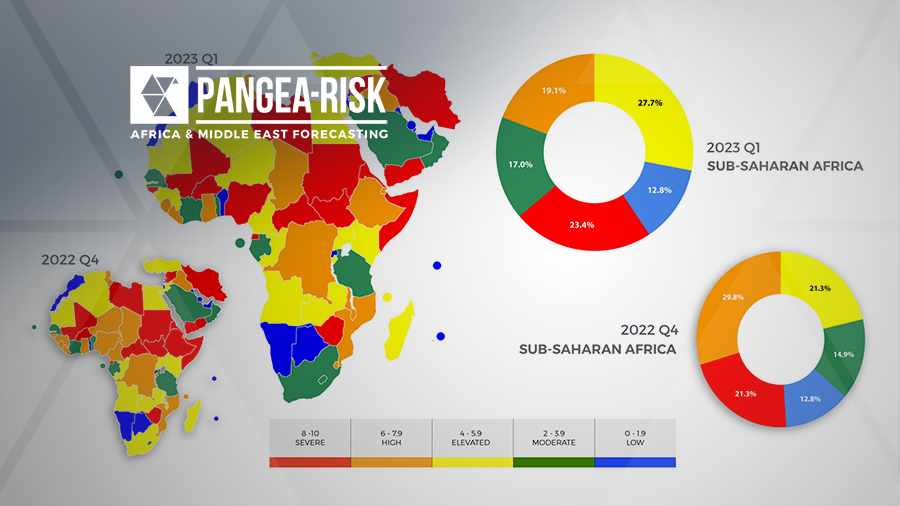

It’s not all doom, gloom, and recession in 2023 – African and Middle East economies will exceed global growth averages on the back of resilient commodity prices. Distressed debt will be treated to avoid chaotic default scenarios, while more foreign investment will return as diverse investors seek higher yield. Maturing democratic systems ensure that socio-economic grievances will increasingly be aired in the political arena, i.e., at elections, rather than on the street. Similarly, some of Africa and the Gulf’s deadliest conflicts will edge towards resolution in 2023. Pangea-Risk identifies some of the most exciting and positive risk trends to look forward to in these regions.