SPECIAL REPORT: THE ‘BATTLE’ FOR SOUTH AFRICA

Mon, 15 June 2020

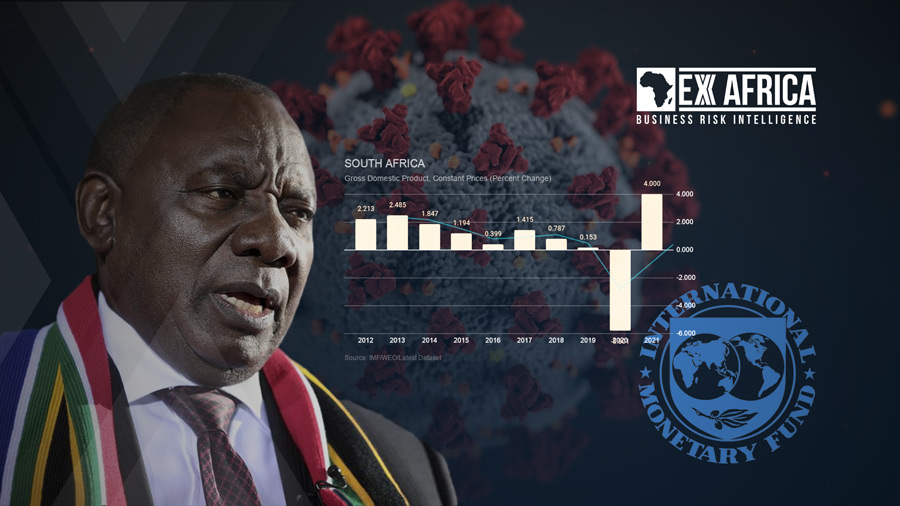

The looming contest over South Africa’s political direction will kick off with a dispute over IMF financial support to plug a massive gap in government revenues. Opponents of IMF conditionalities favour tapping into state pension funds or stepping up central bank bond buying to make up the shortfall. With ‘battle’ lines drawn across the ruling alliance’s ideological divisions, the outcome of the contest will determine the country’s political leadership and economic policy outlook for years to come.