SPECIAL REPORT: TOWARDS ONE MILLION INFECTIONS IN AFRICA

Mon, 27 July 2020

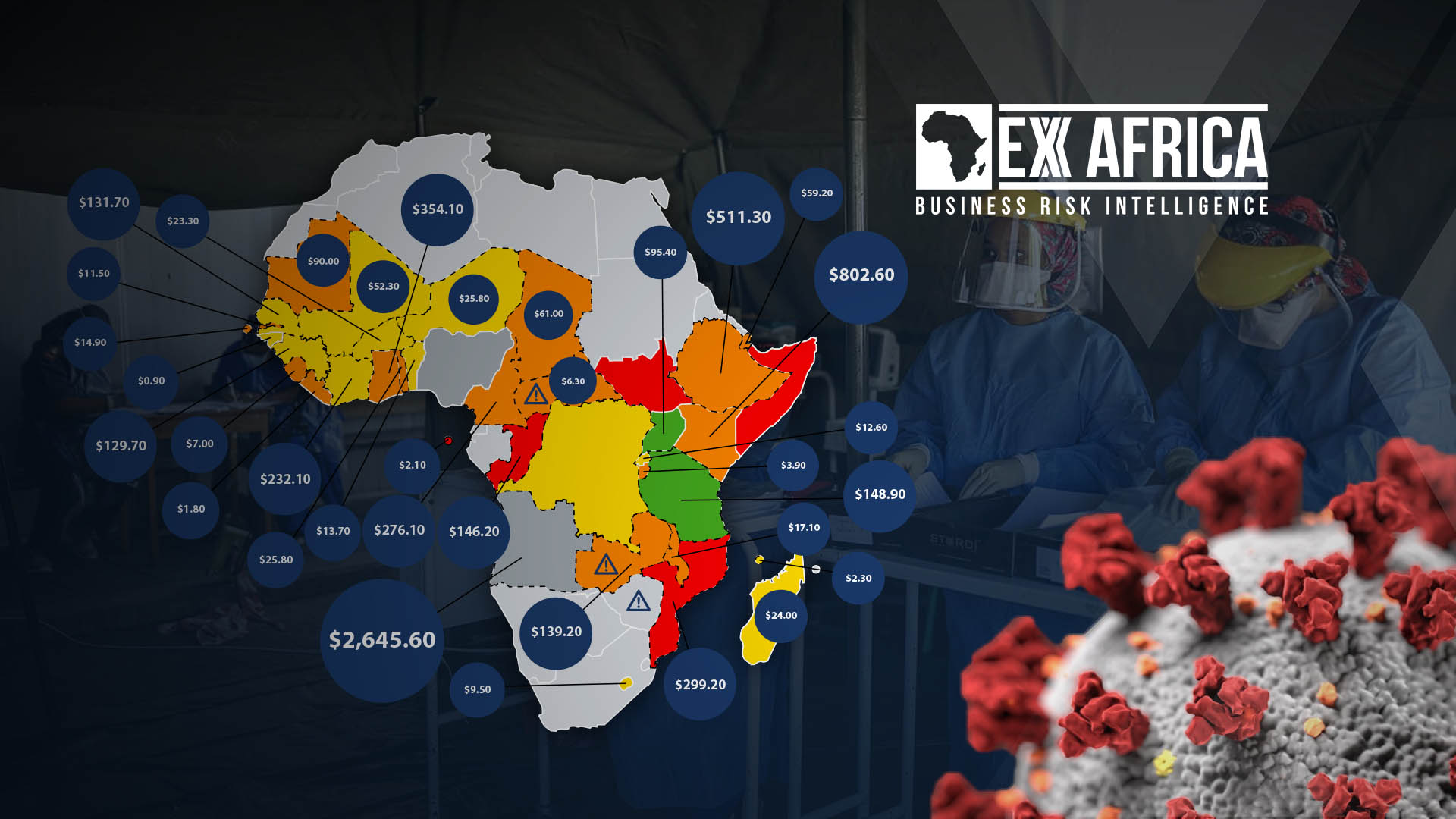

African coronavirus cases will soon reach the one million mark based on the current trajectory of fast rising community transmissions. Prevalent economic optimism and hopes for a recovery next year seem unfounded as budget deficits spiral and new debt obligations balloon. Without further budgetary support, some of Africa’s largest economies are set to default on loan obligations in the coming year.