SPECIAL REPORT: CHANGING TRENDS IN AFRICAN INFRASTRUCTURE FINANCING

Mon, 18 November 2019

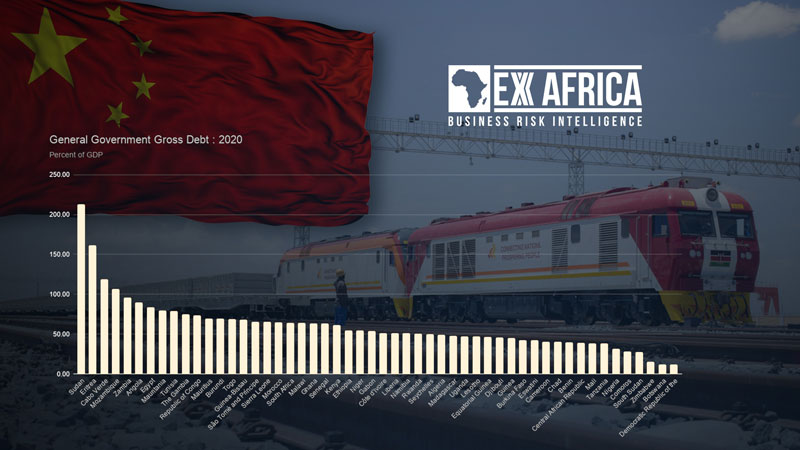

The Chinese government is reassessing its role in landmark infrastructure projects in Africa due to concerns over commercial viability, while some African governments themselves are rejecting Chinese financing conditions. This trend is opening a new avenue for concessional funding and boosting the role of development finance institutions while seeking broader collaboration with commercial institutions.